Business tips

Are tap-to-pay payments safe?

Business tips

There has been a lot of focus in recent years on minimizing physical contact, including in restaurants and retail businesses. In response to the pandemic and customers’ ongoing demands for speed and convenience, tap-to-pay card readers equipped with contactless technology have become commonplace. But is it actually safe when a customer touches their card or mobile phone on a Bluetooth card reader or waves their mobile phone over a terminal?

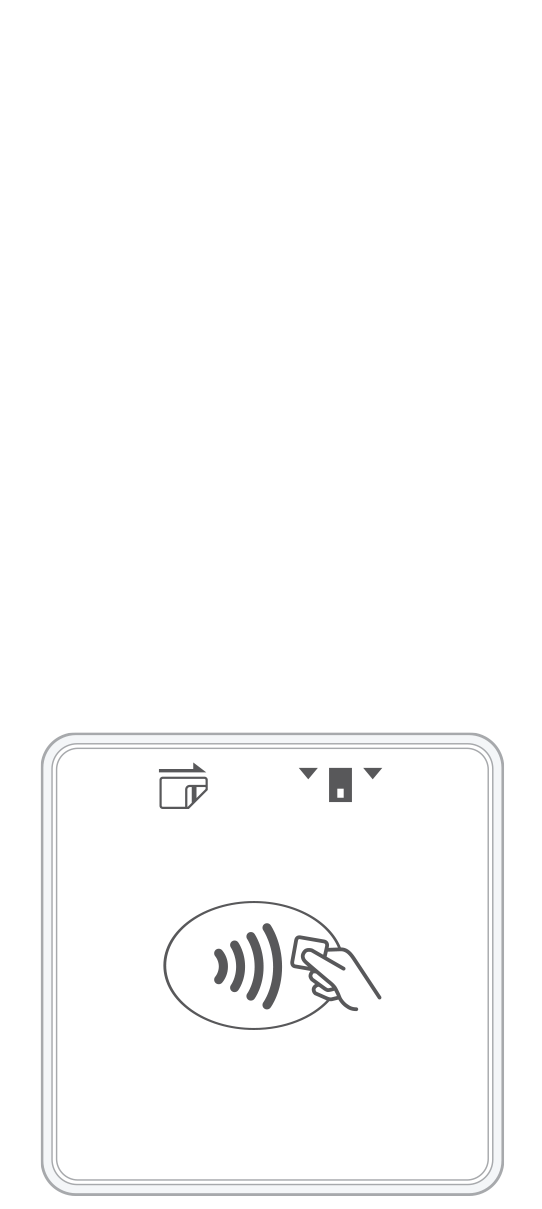

What are tap-to-pay payments?

In simple terms, tap-to-pay or contactless payments contain technology that allows a customer to wave or “tap” their credit or debit card, mobile phone, or wearable device near or on a specific type of reader equipped for the purpose. Never does their plastic card or phone need to leave their possession or be touched by another person or device.

Just how is information transmitted from a chip-enabled card or device to the merchant’s reader? In the case of debit or credit cards, they contain a chip that the issuing bank has preloaded with the customer’s unique payment details. Unlike the magnetic stripe Visa and Mastercards of the past, this sensitive cardholder data cannot be viewed or stolen. Instead, it is encrypted and accessible only to the financial institutions involved in the payment process.

Smartphones, on the other hand, do not have pre-loaded chips. They do, however, contain a digital wallet into which the customer can add information from credit and debit cards, gift cards, tickets, transit passes, etc. The data is then securely stored in the digital wallet and is only accessible at the time of purchase after the customer has authenticated their identity.

Are contactless payments safe? The surprising truth.

In fact, touchless payments are more secure than regular ones. There are several reasons that make this assertion true.

- First and foremost, only the customer can make the tap-to-pay transaction. This is because the digital wallet cannot be opened without the shopper providing biometric or PIN verification that they are indeed who they claim to be. Only once the person’s identity has been verified will the mobile payment system generate a single-use security code that is good for that particular transaction exclusively.

- The physical wallet is no longer necessary. The customer can leave bulky cash and cards at home, carrying only their mobile device or smart credit card. As a result, the buyer is less vulnerable to crime. Furthermore, the digital nature of the transaction means that it will be recorded into the merchant’s point of sale system, with a receipt available either on paper or via email. Should any question arise about the transaction, a record of it will be available for review, reducing the likelihood of misunderstanding or fraud.

- In the event that a card or mobile device is stolen, their information remains impervious to hacking. That’s because data stored on a card’s chip cannot be read by criminals and is accessible only to financial institutions. In terms of smartphones and other mobile devices, the digital wallet is protected from breach with strong passwords and biometric requirements that keep unauthorized users out.

Although the pandemic seems to be subsiding to a certain extent, consumers’ love of making touchless payments looks to be here to stay. Merchants and shoppers alike respond positively to the simplicity, speed, and, dare we say, fun aspects of this revolutionary way to pay. Considering that it is protected behind the scenes with top-of-the-line features that protect merchants and consumers from hackers, the verdict is clear: Tap-to-pay is one of the safest and most effective ways to conclude a purchase currently available to today’s retailers and customers.

Are you ready to begin to accept payments anywhere with contactless transactions in your retail store or restaurant? Just make sure your payment terminal contains the necessary near-field communication (NFC) technology and features the contactless symbol of four curved lines. If it does, it should be able to interface with your customer’s similarly equipped credit card or mobile device.

If your existing card readers and terminals are not already outfitted with NFC technology, talk to your payment processor about upgrading. Having modern payments hardware and software that provides additional ways to pay will offer a whole host of benefits to your and your customers!

Start your Payanywhere account.

Start your Payanywhere account.

3-in-1 Reader |  Terminal |  Keypad |  PINPad Pro |  Flex |  POS+ | |

|---|---|---|---|---|---|---|

Payment types | ||||||

EMV chip card payments (dip) | ||||||

Contactless payments (tap) | ||||||

Magstripe payments (swipe) | ||||||

PIN debit + EBT | ||||||

Device features | ||||||

Built-in barcode scanner | ||||||

Built-in receipt printer | ||||||

Customer-facing second screen | ||||||

External pinpad | ||||||

Wireless use | ||||||

Network | ||||||

Ethernet connectivity | With dock | |||||

Wifi connectivity | ||||||

4G connectivity | ||||||

Pricing | ||||||

Free Placement | ||||||