Business tips

Understanding different types of contactless payments.

Business tips

It is no wonder that contactless payments have seen such an upsurge in popularity over the past few years. Providing shoppers a way to pay for goods and services simply by placing a hand-held or wearable device near a merchant’s compatible reader provides everyone involved with numerous benefits. These include speed, efficiency, convenience, and safety — all without compromising the security or integrity of the transaction.

In 2020, the onset of the coronavirus pandemic gave retailers and shoppers even more reason to look for fast, hygienic payment choices. Even after scientific evidence showed that the virus was not primarily spread through direct contact with surfaces, buyers continued to prefer the contactless experience. In addition, they loved the fact that it could be incorporated into the same mobile card reader technology that enabled them to pay curbside.

Although you may think of the smartphone as the only vehicle for making touchless payments, several other options are proving to be equally popular with buyers and sellers alike. Today’s consumers continue to appreciate the added degree of choice that touchless payments offer now that they are visiting stores in person again.

Debit and credit cards.

Plastic has come a long way since the relatively recent days of the magnetic stripe. As recently as 2015, cards did not have the sophisticated chips that are now required by the major card companies such as Mastercard, American Express, Visa, and Discover. Instead, the cards were still embossed with the customer’s sensitive payment details, information that could easily be stolen by unscrupulous merchants, employees, or common criminals. The dawn of secure EMV chip cards markedly reduced consumers’ vulnerability since information could be stored and encrypted on the small chip embedded in the card. In addition, merchants benefited from the added security, which made them less vulnerable to the financial and legal consequences of data breaches and fraud.

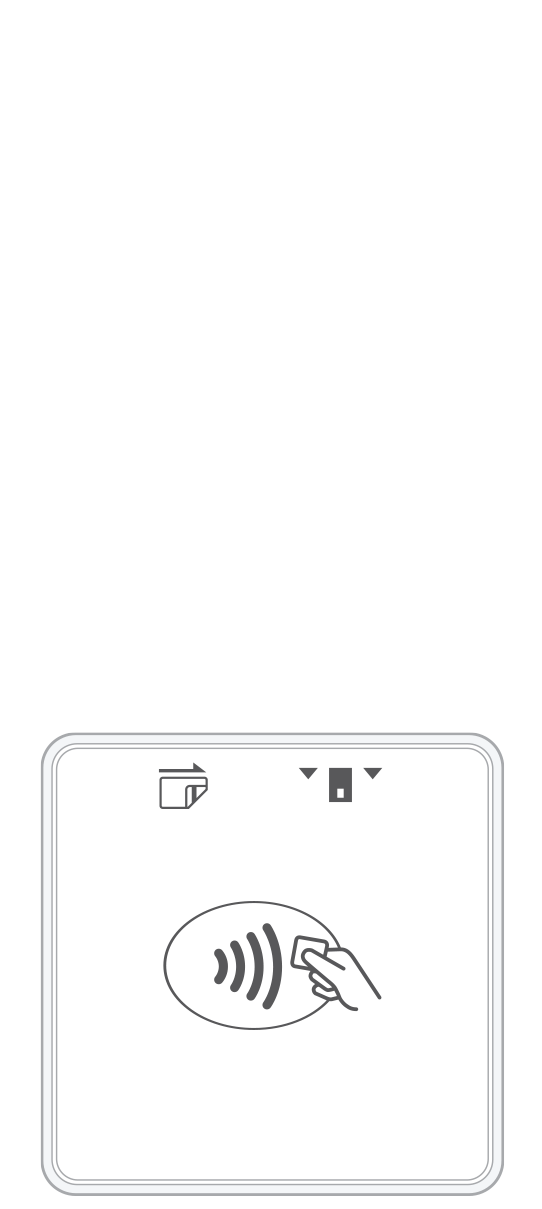

With contactless technology, card users’ payment capabilities have been taken to a new level. Using near field communication (NFC) or radio frequency identification (RFID) capabilities that are included in the card’s antenna and transmitted to the merchant’s reader, information can be safely exchanged instantaneously, allowing for a fast and safe payment experience. Considering the ease and security of these payments, it is no wonder that almost 70 percent of debit card transactions today are conducted contactlessly.

Mobile devices.

Most of today’s consumers would be hard pressed to go anywhere without their smartphones, which they have come to depend on for navigation, communication, entertainment, education, shopping, and more. Using the same technologies mentioned above, smartphones can interface seamlessly with merchants’ compatible terminals and mobile card readers. Thanks to the smartphones that they already carry, shoppers can leave cumbersome wallets, cash, and even plastic cards behind while continuing to enjoy a payment process boasting top-tier security and maximum efficiency.

To make use of their phone’s ability to make contactless payments, a consumer needs to first set up the digital wallet application that is included with both Android and Apple smartphones. Doing so involves following a series of intuitive prompts to add credit card numbers and security codes. Incidentally, the digital wallet can also be used to store loyalty and gift cards, as well as public transportation information. After the consumer has entered the details, they are confirmed with their respective stores and credit card companies before being encrypted and stored in the cloud.

When the time comes to make a purchase, the user simply opens the digital wallet and authenticates their identity through the entry of a passcode, or by providing biometric data such as a fingerprint or face ID. At that point, the shopper needs only to place their smartphone one to two inches from the merchant’s reader for the payment details to be securely transferred and verified.

Wallets such as Apple Pay, Google Wallet, and Samsung Pay are easy to understand and set up even for people who are wary of technology. That may explain why over half of the U.S. shopping population has already embraced mobile payments. In the years to come, it seems quite likely that the adoption of mobile and contactless payments will continue to grow.

Smartwatches.

Today’s smartwatches do much more than simply tell the time. In many respects, they are mini mobile phones that include a wide array of their counterpart’s capabilities, as well as additional features such as fitness and health monitoring. Because digital wallets sync seamlessly with smartphones, the smart Apple or Android timepiece can also be effectively used to pay for goods and services.

The watch takes convenience one step further by removing the necessity of grabbing a phone from a purse or pocket to make a payment. Instead, a consumer needs only to make a couple of taps to achieve the same security and transaction speed.

Key fobs.

Key fobs give consumers yet another payment option that attaches easily to a key-ring they may already be using to access their home or start their car. Many credit card companies offer their cards in key fob form as a supplement to or instead of a traditional piece of plastic that goes in the wallet. Once again, this alternative format helps to make carrying the traditional wallet less necessary. As a result, shoppers can submit safe and secure payments on the go without being bogged down by purses or wallets.

Embed This Infographic

Copy and paste the code below to get this infographic onto your website or blog.

Related Reading

Start your Payanywhere account.

Start your Payanywhere account.

3-in-1 Reader |  Terminal |  Keypad |  PINPad Pro |  Flex |  POS+ | |

|---|---|---|---|---|---|---|

Payment types | ||||||

EMV chip card payments (dip) | ||||||

Contactless payments (tap) | ||||||

Magstripe payments (swipe) | ||||||

PIN debit + EBT | ||||||

Device features | ||||||

Built-in barcode scanner | ||||||

Built-in receipt printer | ||||||

Customer-facing second screen | ||||||

External pinpad | ||||||

Wireless use | ||||||

Network | ||||||

Ethernet connectivity | With dock | |||||

Wifi connectivity | ||||||

4G connectivity | ||||||

Pricing | ||||||

Free Placement | ||||||