Business tips

10 things to know about NFC contactless payments.

Business tips

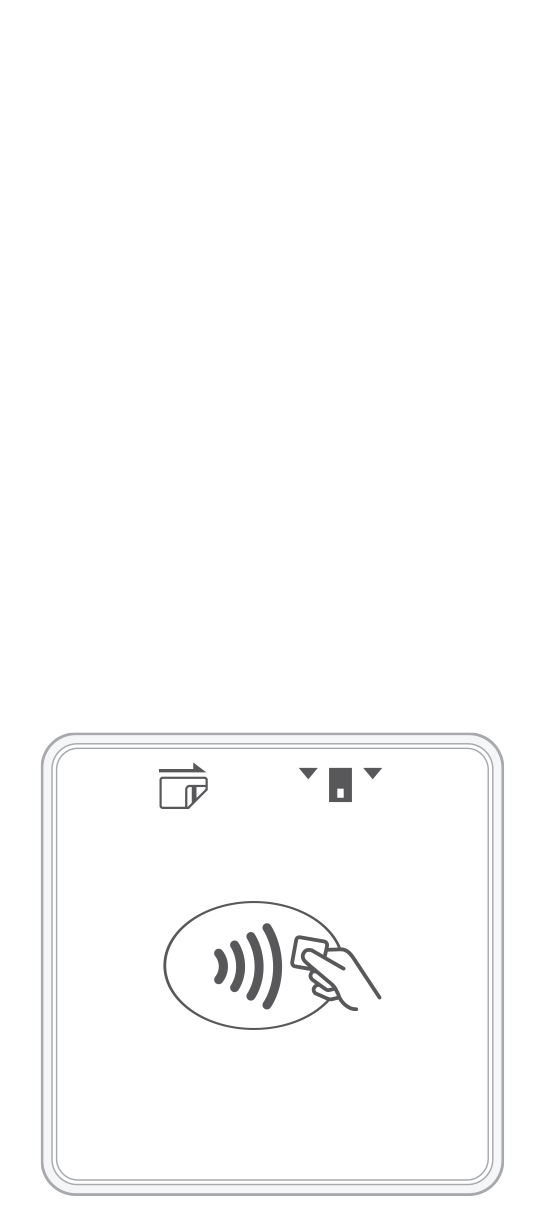

Thanks to a technology known as near-field communications (NFC), it is possible for customers to make payments either via a smartphone or a chip-enabled credit card without the merchant ever needing to handle their card. The magic happens via either a digital wallet application like Apple Pay or Samsung Pay on the customer’s mobile device or a chip that is embedded into a physical card. NFC contactless payments are not only effortless in their execution, they are also safe and secure. Therefore, it is no wonder that they gain more popularity with U.S. shoppers with each passing year.

The ease of use is quite apparent to buyers, but merchants are also discovering how modern technology is making the contactless payment experience as smooth as silk. The same small NFC-equipped card reader that a buyer “taps” with their chip card can also contain software that interfaces with both Apple and Android smartphones. As a result, customers get the payment flexibility they desire, and sellers are rewarded with return visits from these satisfied individuals. In addition, sellers can breathe easier knowing that their systems are PCI-compliant with the data security standards that have been set forth by the payment card industry.

In addition to being easy to use, the security of NFC contactless payments is unparalleled. This is because each transaction is a separate entity unto itself, making fraud infinitely more difficult to carry out. When a customer places their card near a contactless reader, a single-use token is created that represents the person’s unique credit card information. Once the verification and authorization process is completed, the token becomes null and void. In a similar way, a buyer’s credentials are protected when they make contactless payments using a smartphone that is equipped with a digital wallet application. However, when using a digital wallet, even more verification is required — via a signature, PIN, or even biometric identification.

Anyone who has languished in a long checkout line knows how endlessly the payment process can drag on. No doubt, it seemed like hours were passing as the customers ahead of you fumbled for their cash or cards or agonized over writing a check. Fortunately, contactless technology is turning the formerly slow shuffle at the register into a steady trot. In fact, the process takes about half as much time as a traditional credit card purchase.

These benefits are not lost on shoppers. Although U.S. consumers took some time to embrace NFC contactless technology at first, its popularity is now skyrocketing. Considering that virtually everyone carries their mobile phones with them and more and more Americans are getting NFC cards, this trend will only continue in the years to come.

NFC contactless readers use encryption to keep customers’ information secure. This involves transforming information into a format that looks like gibberish to anyone who does not have the means to decode it. Encrypted data is then “tokenized” or transformed into a randomly generated, algorithmic representation of a customer’s credit card account number. This token can be stored in digital wallets, in point-of-sale solutions, or can be used in ecommerce systems to prevent the sensitive information on the card from being exposed to fraud. If you’re partnering with a reputable merchant services provider, they’ll be offering you solutions that utilize the latest in encryption and tokenization to keep you in compliance with the payment card industry’s digital security standards and protected from liability.

Although the individual time savings that each customer realizes at the register is only a matter of a few seconds, everyone wins with NFC contactless payments. For one thing, customers are able to go on with their lives more quickly. Meanwhile, from the merchant’s point of view, a day’s worth of these minor gains can add up over time.

When customers were first introduced to the idea of contactless payments, many people wondered if the information stored in digital wallets could be surreptitiously stolen by fraudsters. For instance, could a criminal stealthily place a reader in close proximity to a phone equipped with Apple Pay or Android Pay and thereby initiate a payment? As it turns out, this is not possible. For one thing, the wallet and the reader must be in very close proximity to each other. More importantly, the contactless process requires authentication with a PIN or fingerprint, something that a fraudster could not easily provide.

However, let’s say the worst happens and a hacker somehow obtains the information that has been tokenized. Because tokens are used only once and are then destroyed, there is no danger of a consumer experiencing long-term, serious consequences.

Of course, there are still many buyers who insist on continuing to make payments using cash or magstripe credit cards. It may be quite some time before everyone recognizes the processing speed and security advantages involved in utilizing NFC contactless payments. Fortunately, modern systems are nimble and can easily evolve according to individual customer needs.

Even when customers visit drive-through environments and pay for products and services on the fly, they are seeing a significant streamlining of the payment process. In a world where every minute seems to count and patience is at a premium, even the savings of a few seconds can turn into an important advantage.

Embed This Infographic

Copy and paste the code below to get this infographic onto your website or blog.

More from Business tips

Start your Payanywhere account.

Start your Payanywhere account.

3-in-1 Reader |  Terminal |  Keypad |  PINPad Pro |  Flex |  POS+ | |

|---|---|---|---|---|---|---|

Payment types | ||||||

EMV chip card payments (dip) | ||||||

Contactless payments (tap) | ||||||

Magstripe payments (swipe) | ||||||

PIN debit + EBT | ||||||

Device features | ||||||

Built-in barcode scanner | ||||||

Built-in receipt printer | ||||||

Customer-facing second screen | ||||||

External pinpad | ||||||

Wireless use | ||||||

Network | ||||||

Ethernet connectivity | With dock | |||||

Wifi connectivity | ||||||

4G connectivity | ||||||

Pricing | ||||||

Free Placement | ||||||